gamCopula: Generalized Additive Models for Bivariate Conditional Dependence Structures and Vine Copulas

Source:R/gamCopula-package.R

gamCopula-package.RdThis package implements inference and simulation tools to apply generalized additive models to bivariate dependence structures and vine copulas.

Details

More details can be found in Vatter and Chavez-Demoulin (2015) and Vatter and Nagler (2016).

| Package: | gamCopula |

| Type: | Package |

| Version: | 0.0-8 |

| Date: | 2025-04-02 |

| License: | GPL-3 |

References

Aas, K., C. Czado, A. Frigessi, and H. Bakken (2009) Pair-copula constructions of multiple dependence. Insurance: Mathematics and Economics, 44(2), 182–198.

Brechmann, E. C., C. Czado, and K. Aas (2012) Truncated regular vines in high dimensions with applications to financial data. Canadian Journal of Statistics, 40(1), 68–85.

Dissmann, J. F., E. C. Brechmann, C. Czado, and D. Kurowicka (2013) Selecting and estimating regular vine copulae and application to financial returns. Computational Statistics & Data Analysis, 59(1), 52–69.

Vatter, T. and V. Chavez-Demoulin (2015) Generalized Additive Models for Conditional Dependence Structures. Journal of Multivariate Analysis, 141, 147–167.

Vatter, T. and T. Nagler (2016) Generalized additive models for non-simplified pair-copula constructions. https://arxiv.org/abs/1608.01593

Wood, S. N. (2004) Stable and efficient multiple smoothing parameter estimation for generalized additive models. Journal of the American Statistical Association, 99, 673–686.

Wood, S. N. (2006) Generalized Additive Models: an introduction with R. Chapman and Hall/CRC.

See also

The present package heavily relies on the mgcv and VineCopula packages, as it basically extends and mixes both of them.

Examples

##### A gamBiCop example

require(copula)

require(mgcv)

set.seed(0)

## Simulation parameters (sample size, correlation between covariates,

## Gaussian copula family)

n <- 5e2

rho <- 0.5

fam <- 1

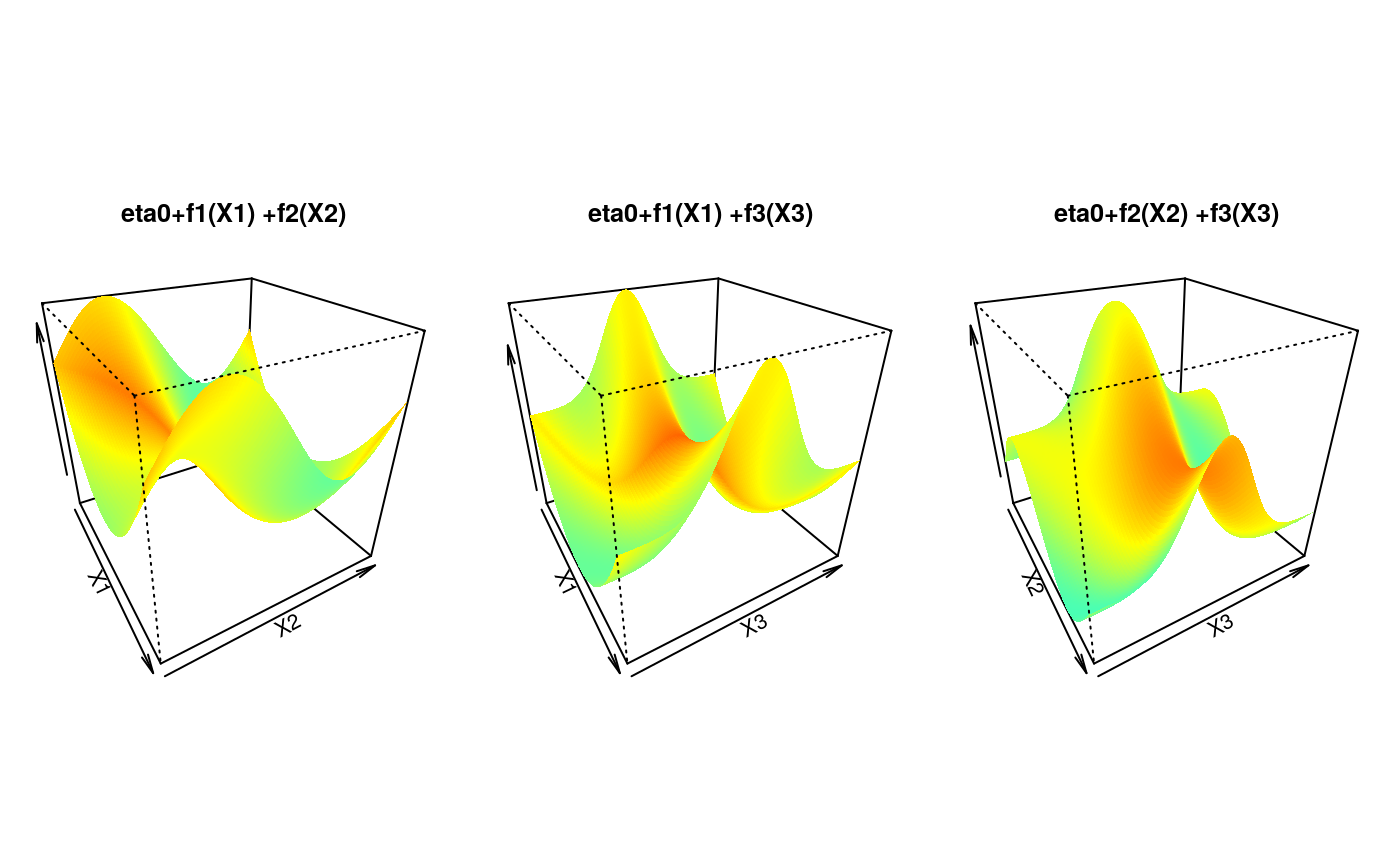

### A calibration surface depending on three variables

eta0 <- 1

calib.surf <- list(

calib.quad <- function(t, Ti = 0, Tf = 1, b = 8) {

Tm <- (Tf - Ti) / 2

a <- -(b / 3) * (Tf^2 - 3 * Tf * Tm + 3 * Tm^2)

return(a + b * (t - Tm)^2)

},

calib.sin <- function(t, Ti = 0, Tf = 1, b = 1, f = 1) {

a <- b * (1 - 2 * Tf * pi / (f * Tf * pi +

cos(2 * f * pi * (Tf - Ti))

- cos(2 * f * pi * Ti)))

return((a + b) / 2 + (b - a) * sin(2 * f * pi * (t - Ti)) / 2)

},

calib.exp <- function(t, Ti = 0, Tf = 1, b = 2, s = Tf / 8) {

Tm <- (Tf - Ti) / 2

a <- (b * s * sqrt(2 * pi) / Tf) * (pnorm(0, Tm, s) - pnorm(Tf, Tm, s))

return(a + b * exp(-(t - Tm)^2 / (2 * s^2)))

}

)

### Display the calibration surface

par(mfrow = c(1, 3), pty = "s", mar = c(1, 1, 4, 1))

u <- seq(0, 1, length.out = 100)

sel <- matrix(c(1, 1, 2, 2, 3, 3), ncol = 2)

jet.colors <- colorRamp(c(

"#00007F", "blue", "#007FFF", "cyan", "#7FFF7F",

"yellow", "#FF7F00", "red", "#7F0000"

))

jet <- function(x) {

rgb(jet.colors(exp(x / 3) / (1 + exp(x / 3))),

maxColorValue = 255

)

}

for (k in 1:3) {

tmp <- outer(u, u, function(x, y) {

eta0 + calib.surf[[sel[k, 1]]](x) + calib.surf[[sel[k, 2]]](y)

})

persp(u, u, tmp,

border = NA, theta = 60, phi = 30, zlab = "",

col = matrix(jet(tmp), nrow = 100),

xlab = paste("X", sel[k, 1], sep = ""),

ylab = paste("X", sel[k, 2], sep = ""),

main = paste("eta0+f", sel[k, 1],

"(X", sel[k, 1], ") +f", sel[k, 2],

"(X", sel[k, 2], ")",

sep = ""

)

)

}

### 3-dimensional matrix X of covariates

covariates.distr <- mvdc(normalCopula(rho, dim = 3),

c("unif"), list(list(min = 0, max = 1)),

marginsIdentical = TRUE

)

X <- rMvdc(n, covariates.distr)

### U in [0,1]x[0,1] with copula parameter depending on X

U <- condBiCopSim(fam, function(x1, x2, x3) {

eta0 + sum(mapply(function(f, x) {

f(x)

}, calib.surf, c(x1, x2, x3)))

}, X[, 1:3], par2 = 6, return.par = TRUE)

### Merge U and X

data <- data.frame(U$data, X)

names(data) <- c(paste("u", 1:2, sep = ""), paste("x", 1:3, sep = ""))

### Display the data

dev.off()

#> null device

#> 1

plot(data[, "u1"], data[, "u2"], xlab = "U1", ylab = "U2")

### Model fit with a basis size (arguably) too small

### and unpenalized cubic spines

pen <- FALSE

basis0 <- c(3, 4, 4)

formula <- ~ s(x1, k = basis0[1], bs = "cr", fx = !pen) +

s(x2, k = basis0[2], bs = "cr", fx = !pen) +

s(x3, k = basis0[3], bs = "cr", fx = !pen)

system.time(fit0 <- gamBiCopFit(data, formula, fam))

#> user system elapsed

#> 0.097 0.000 0.097

### Model fit with a better basis size and penalized cubic splines (via min GCV)

pen <- TRUE

basis1 <- c(3, 10, 10)

formula <- ~ s(x1, k = basis1[1], bs = "cr", fx = !pen) +

s(x2, k = basis1[2], bs = "cr", fx = !pen) +

s(x3, k = basis1[3], bs = "cr", fx = !pen)

system.time(fit1 <- gamBiCopFit(data, formula, fam))

#> user system elapsed

#> 0.456 1.535 0.358

### Extract the gamBiCop objects and show various methods

(res <- sapply(list(fit0, fit1), function(fit) {

fit$res

}))

#> [[1]]

#> Gaussian copula with tau(z) = (exp(z)-1)/(exp(z)+1) where

#> z ~ s(x1, k = basis0[1], bs = "cr", fx = !pen) + s(x2, k = basis0[2],

#> bs = "cr", fx = !pen) + s(x3, k = basis0[3], bs = "cr", fx = !pen)

#>

#> [[2]]

#> Gaussian copula with tau(z) = (exp(z)-1)/(exp(z)+1) where

#> z ~ s(x1, k = basis1[1], bs = "cr", fx = !pen) + s(x2, k = basis1[2],

#> bs = "cr", fx = !pen) + s(x3, k = basis1[3], bs = "cr", fx = !pen)

#>

metds <- list("logLik" = logLik, "AIC" = AIC, "BIC" = BIC, "EDF" = EDF)

lapply(res, function(x) sapply(metds, function(f) f(x)))

#> [[1]]

#> [[1]]$logLik

#> 'log Lik.' 266.8974 (df=9)

#>

#> [[1]]$AIC

#> [1] -515.7948

#>

#> [[1]]$BIC

#> [1] -477.8633

#>

#> [[1]]$EDF

#> [1] 1 2 3 3

#>

#>

#> [[2]]

#> [[2]]$logLik

#> 'log Lik.' 302.9581 (df=16.24202)

#>

#> [[2]]$AIC

#> [1] -573.4321

#>

#> [[2]]$BIC

#> [1] -504.9783

#>

#> [[2]]$EDF

#> [1] 1.000000 1.999178 7.577543 5.665301

#>

#>

### Comparison between fitted, true smooth and spline approximation for each

### true smooth function for the two basis sizes

fitted <- lapply(res, function(x) {

gamBiCopPredict(x, data.frame(x1 = u, x2 = u, x3 = u),

type = "terms"

)$calib

})

true <- vector("list", 3)

for (i in 1:3) {

y <- eta0 + calib.surf[[i]](u)

true[[i]]$true <- y - eta0

temp <- gam(y ~ s(u, k = basis0[i], bs = "cr", fx = TRUE))

true[[i]]$approx <- predict.gam(temp, type = "terms")

temp <- gam(y ~ s(u, k = basis1[i], bs = "cr", fx = FALSE))

true[[i]]$approx2 <- predict.gam(temp, type = "terms")

}

### Display results

par(mfrow = c(1, 3), pty = "s")

yy <- range(true, fitted)

yy[1] <- yy[1] * 1.5

for (k in 1:3) {

plot(u, true[[k]]$true,

type = "l", ylim = yy,

xlab = paste("Covariate", k), ylab = paste("Smooth", k)

)

lines(u, true[[k]]$approx, col = "red", lty = 2)

lines(u, fitted[[1]][, k], col = "red")

lines(u, fitted[[2]][, k], col = "green")

lines(u, true[[k]]$approx2, col = "green", lty = 2)

legend("bottomleft",

cex = 0.6, lty = c(1, 1, 2, 1, 2),

c("True", "Fitted", "Appox 1", "Fitted 2", "Approx 2"),

col = c("black", "red", "red", "green", "green")

)

}

###### A gamVine example

set.seed(0)

### Simulation parameters

## Sample size

n <- 1e3

## Copula families

familyset <- c(1:2, 301:304, 401:404)

## Define a 4-dimensional R-vine tree structure matrix

d <- 4

Matrix <- c(2, 3, 4, 1, 0, 3, 4, 1, 0, 0, 4, 1, 0, 0, 0, 1)

Matrix <- matrix(Matrix, d, d)

nnames <- paste("X", 1:d, sep = "")

### A function factory

eta0 <- 1

calib.surf <- list(

calib.quad <- function(t, Ti = 0, Tf = 1, b = 8) {

Tm <- (Tf - Ti) / 2

a <- -(b / 3) * (Tf^2 - 3 * Tf * Tm + 3 * Tm^2)

return(a + b * (t - Tm)^2)

},

calib.sin <- function(t, Ti = 0, Tf = 1, b = 1, f = 1) {

a <- b * (1 - 2 * Tf * pi / (f * Tf * pi +

cos(2 * f * pi * (Tf - Ti))

- cos(2 * f * pi * Ti)))

return((a + b) / 2 + (b - a) * sin(2 * f * pi * (t - Ti)) / 2)

},

calib.exp <- function(t, Ti = 0, Tf = 1, b = 2, s = Tf / 8) {

Tm <- (Tf - Ti) / 2

a <- (b * s * sqrt(2 * pi) / Tf) * (pnorm(0, Tm, s) - pnorm(Tf, Tm, s))

return(a + b * exp(-(t - Tm)^2 / (2 * s^2)))

}

)

### Create the model

## Define gam-vine model list

count <- 1

model <- vector(mode = "list", length = d * (d - 1) / 2)

sel <- seq(d, d^2 - d, by = d)

## First tree

for (i in 1:(d - 1)) {

# Select a copula family

family <- sample(familyset, 1)

model[[count]]$family <- family

# Use the canonical link and a randomly generated parameter

if (is.element(family, c(1, 2))) {

model[[count]]$par <- tanh(rnorm(1) / 2)

if (family == 2) {

model[[count]]$par2 <- 2 + exp(rnorm(1))

}

} else {

if (is.element(family, c(401:404))) {

rr <- rnorm(1)

model[[count]]$par <- sign(rr) * (1 + abs(rr))

} else {

model[[count]]$par <- rnorm(1)

}

model[[count]]$par2 <- 0

}

count <- count + 1

}

## A dummy dataset

data <- data.frame(u1 = runif(1e2), u2 = runif(1e2), matrix(runif(1e2 * d), 1e2, d))

## Trees 2 to (d-1)

for (j in 2:(d - 1)) {

for (i in 1:(d - j)) {

# Select a copula family

family <- sample(familyset, 1)

# Select the conditiong set and create a model formula

cond <- nnames[sort(Matrix[(d - j + 2):d, i])]

tmpform <- paste("~", paste(paste("s(", cond, ", k=10, bs='cr')",

sep = ""

), collapse = " + "))

l <- length(cond)

temp <- sample(3, l, replace = TRUE)

# Spline approximation of the true function

m <- 1e2

x <- matrix(seq(0, 1, length.out = m), nrow = m, ncol = 1)

if (l != 1) {

tmp.fct <- paste("function(x){eta0+",

paste(sapply(1:l, function(x) {

paste("calib.surf[[", temp[x], "]](x[", x, "])",

sep = ""

)

}), collapse = "+"), "}",

sep = ""

)

tmp.fct <- eval(parse(text = tmp.fct))

x <- eval(parse(text = paste0("expand.grid(",

paste0(rep("x", l), collapse = ","), ")",

collapse = ""

)))

y <- apply(x, 1, tmp.fct)

} else {

tmp.fct <- function(x) eta0 + calib.surf[[temp]](x)

colnames(x) <- cond

y <- tmp.fct(x)

}

# Estimate the gam model

form <- as.formula(paste0("y", tmpform))

dd <- data.frame(y, x)

names(dd) <- c("y", cond)

b <- gam(form, data = dd)

# plot(x[,1],(y-fitted(b))/y)

# Create a dummy gamBiCop object

tmp <- gamBiCopFit(data = data, formula = form, family = 1, n.iters = 1)$res

# Update the copula family and the model coefficients

attr(tmp, "model")$coefficients <- coefficients(b)

attr(tmp, "model")$smooth <- b$smooth

attr(tmp, "family") <- family

if (family == 2) {

attr(tmp, "par2") <- 2 + exp(rnorm(1))

}

model[[count]] <- tmp

count <- count + 1

}

}

## Create the gamVineCopula object

GVC <- gamVine(Matrix = Matrix, model = model, names = nnames)

print(GVC)

#> GAM-Vine matrix:

#> [,1] [,2] [,3] [,4]

#> [1,] 2 0 0 0

#> [2,] 3 3 0 0

#> [3,] 4 4 4 0

#> [4,] 1 1 1 1

#>

#> Where

#> 1 <-> X1

#> 2 <-> X2

#> 3 <-> X3

#> 4 <-> X4

#>

#> Tree 1:

#> X2,X1: Gumbel type 3 (survival and 90 degrees rotated)

#> X3,X1: Gaussian

#> X4,X1: Gumbel type 1 (standard and 90 degrees rotated)

#>

#> Tree 2:

#> X2,X4|X1 : Gumbel type 1 (standard and 90 degrees rotated) copula with tau(z) = (exp(z)-1)/(exp(z)+1) where

#> z ~ s(X1, k = 10, bs = "cr")

#> X3,X4|X1 : Gumbel type 2 (standard and 270 degrees rotated) copula with tau(z) = (exp(z)-1)/(exp(z)+1) where

#> z ~ s(X1, k = 10, bs = "cr")

#>

#> Tree 3:

#> X2,X3|X4,X1 : Gumbel type 4 (survival and 270 degrees rotated) copula with tau(z) = (exp(z)-1)/(exp(z)+1) where

#> z ~ s(X1, k = 10, bs = "cr") + s(X4, k = 10, bs = "cr")

#

if (FALSE) { # \dontrun{

### Simulate and fit the model

sim <- gamVineSimulate(n, GVC)

fitGVC <- gamVineSeqFit(sim, GVC, verbose = TRUE)

fitGVC2 <- gamVineCopSelect(sim, Matrix, verbose = TRUE)

### Plot the results

par(mfrow = c(3, 4))

plot(GVC, ylim = c(-2.5, 2.5))

plot(fitGVC, ylim = c(-2.5, 2.5))

plot(fitGVC2, ylim = c(-2.5, 2.5))

} # }

### 3-dimensional matrix X of covariates

covariates.distr <- mvdc(normalCopula(rho, dim = 3),

c("unif"), list(list(min = 0, max = 1)),

marginsIdentical = TRUE

)

X <- rMvdc(n, covariates.distr)

### U in [0,1]x[0,1] with copula parameter depending on X

U <- condBiCopSim(fam, function(x1, x2, x3) {

eta0 + sum(mapply(function(f, x) {

f(x)

}, calib.surf, c(x1, x2, x3)))

}, X[, 1:3], par2 = 6, return.par = TRUE)

### Merge U and X

data <- data.frame(U$data, X)

names(data) <- c(paste("u", 1:2, sep = ""), paste("x", 1:3, sep = ""))

### Display the data

dev.off()

#> null device

#> 1

plot(data[, "u1"], data[, "u2"], xlab = "U1", ylab = "U2")

### Model fit with a basis size (arguably) too small

### and unpenalized cubic spines

pen <- FALSE

basis0 <- c(3, 4, 4)

formula <- ~ s(x1, k = basis0[1], bs = "cr", fx = !pen) +

s(x2, k = basis0[2], bs = "cr", fx = !pen) +

s(x3, k = basis0[3], bs = "cr", fx = !pen)

system.time(fit0 <- gamBiCopFit(data, formula, fam))

#> user system elapsed

#> 0.097 0.000 0.097

### Model fit with a better basis size and penalized cubic splines (via min GCV)

pen <- TRUE

basis1 <- c(3, 10, 10)

formula <- ~ s(x1, k = basis1[1], bs = "cr", fx = !pen) +

s(x2, k = basis1[2], bs = "cr", fx = !pen) +

s(x3, k = basis1[3], bs = "cr", fx = !pen)

system.time(fit1 <- gamBiCopFit(data, formula, fam))

#> user system elapsed

#> 0.456 1.535 0.358

### Extract the gamBiCop objects and show various methods

(res <- sapply(list(fit0, fit1), function(fit) {

fit$res

}))

#> [[1]]

#> Gaussian copula with tau(z) = (exp(z)-1)/(exp(z)+1) where

#> z ~ s(x1, k = basis0[1], bs = "cr", fx = !pen) + s(x2, k = basis0[2],

#> bs = "cr", fx = !pen) + s(x3, k = basis0[3], bs = "cr", fx = !pen)

#>

#> [[2]]

#> Gaussian copula with tau(z) = (exp(z)-1)/(exp(z)+1) where

#> z ~ s(x1, k = basis1[1], bs = "cr", fx = !pen) + s(x2, k = basis1[2],

#> bs = "cr", fx = !pen) + s(x3, k = basis1[3], bs = "cr", fx = !pen)

#>

metds <- list("logLik" = logLik, "AIC" = AIC, "BIC" = BIC, "EDF" = EDF)

lapply(res, function(x) sapply(metds, function(f) f(x)))

#> [[1]]

#> [[1]]$logLik

#> 'log Lik.' 266.8974 (df=9)

#>

#> [[1]]$AIC

#> [1] -515.7948

#>

#> [[1]]$BIC

#> [1] -477.8633

#>

#> [[1]]$EDF

#> [1] 1 2 3 3

#>

#>

#> [[2]]

#> [[2]]$logLik

#> 'log Lik.' 302.9581 (df=16.24202)

#>

#> [[2]]$AIC

#> [1] -573.4321

#>

#> [[2]]$BIC

#> [1] -504.9783

#>

#> [[2]]$EDF

#> [1] 1.000000 1.999178 7.577543 5.665301

#>

#>

### Comparison between fitted, true smooth and spline approximation for each

### true smooth function for the two basis sizes

fitted <- lapply(res, function(x) {

gamBiCopPredict(x, data.frame(x1 = u, x2 = u, x3 = u),

type = "terms"

)$calib

})

true <- vector("list", 3)

for (i in 1:3) {

y <- eta0 + calib.surf[[i]](u)

true[[i]]$true <- y - eta0

temp <- gam(y ~ s(u, k = basis0[i], bs = "cr", fx = TRUE))

true[[i]]$approx <- predict.gam(temp, type = "terms")

temp <- gam(y ~ s(u, k = basis1[i], bs = "cr", fx = FALSE))

true[[i]]$approx2 <- predict.gam(temp, type = "terms")

}

### Display results

par(mfrow = c(1, 3), pty = "s")

yy <- range(true, fitted)

yy[1] <- yy[1] * 1.5

for (k in 1:3) {

plot(u, true[[k]]$true,

type = "l", ylim = yy,

xlab = paste("Covariate", k), ylab = paste("Smooth", k)

)

lines(u, true[[k]]$approx, col = "red", lty = 2)

lines(u, fitted[[1]][, k], col = "red")

lines(u, fitted[[2]][, k], col = "green")

lines(u, true[[k]]$approx2, col = "green", lty = 2)

legend("bottomleft",

cex = 0.6, lty = c(1, 1, 2, 1, 2),

c("True", "Fitted", "Appox 1", "Fitted 2", "Approx 2"),

col = c("black", "red", "red", "green", "green")

)

}

###### A gamVine example

set.seed(0)

### Simulation parameters

## Sample size

n <- 1e3

## Copula families

familyset <- c(1:2, 301:304, 401:404)

## Define a 4-dimensional R-vine tree structure matrix

d <- 4

Matrix <- c(2, 3, 4, 1, 0, 3, 4, 1, 0, 0, 4, 1, 0, 0, 0, 1)

Matrix <- matrix(Matrix, d, d)

nnames <- paste("X", 1:d, sep = "")

### A function factory

eta0 <- 1

calib.surf <- list(

calib.quad <- function(t, Ti = 0, Tf = 1, b = 8) {

Tm <- (Tf - Ti) / 2

a <- -(b / 3) * (Tf^2 - 3 * Tf * Tm + 3 * Tm^2)

return(a + b * (t - Tm)^2)

},

calib.sin <- function(t, Ti = 0, Tf = 1, b = 1, f = 1) {

a <- b * (1 - 2 * Tf * pi / (f * Tf * pi +

cos(2 * f * pi * (Tf - Ti))

- cos(2 * f * pi * Ti)))

return((a + b) / 2 + (b - a) * sin(2 * f * pi * (t - Ti)) / 2)

},

calib.exp <- function(t, Ti = 0, Tf = 1, b = 2, s = Tf / 8) {

Tm <- (Tf - Ti) / 2

a <- (b * s * sqrt(2 * pi) / Tf) * (pnorm(0, Tm, s) - pnorm(Tf, Tm, s))

return(a + b * exp(-(t - Tm)^2 / (2 * s^2)))

}

)

### Create the model

## Define gam-vine model list

count <- 1

model <- vector(mode = "list", length = d * (d - 1) / 2)

sel <- seq(d, d^2 - d, by = d)

## First tree

for (i in 1:(d - 1)) {

# Select a copula family

family <- sample(familyset, 1)

model[[count]]$family <- family

# Use the canonical link and a randomly generated parameter

if (is.element(family, c(1, 2))) {

model[[count]]$par <- tanh(rnorm(1) / 2)

if (family == 2) {

model[[count]]$par2 <- 2 + exp(rnorm(1))

}

} else {

if (is.element(family, c(401:404))) {

rr <- rnorm(1)

model[[count]]$par <- sign(rr) * (1 + abs(rr))

} else {

model[[count]]$par <- rnorm(1)

}

model[[count]]$par2 <- 0

}

count <- count + 1

}

## A dummy dataset

data <- data.frame(u1 = runif(1e2), u2 = runif(1e2), matrix(runif(1e2 * d), 1e2, d))

## Trees 2 to (d-1)

for (j in 2:(d - 1)) {

for (i in 1:(d - j)) {

# Select a copula family

family <- sample(familyset, 1)

# Select the conditiong set and create a model formula

cond <- nnames[sort(Matrix[(d - j + 2):d, i])]

tmpform <- paste("~", paste(paste("s(", cond, ", k=10, bs='cr')",

sep = ""

), collapse = " + "))

l <- length(cond)

temp <- sample(3, l, replace = TRUE)

# Spline approximation of the true function

m <- 1e2

x <- matrix(seq(0, 1, length.out = m), nrow = m, ncol = 1)

if (l != 1) {

tmp.fct <- paste("function(x){eta0+",

paste(sapply(1:l, function(x) {

paste("calib.surf[[", temp[x], "]](x[", x, "])",

sep = ""

)

}), collapse = "+"), "}",

sep = ""

)

tmp.fct <- eval(parse(text = tmp.fct))

x <- eval(parse(text = paste0("expand.grid(",

paste0(rep("x", l), collapse = ","), ")",

collapse = ""

)))

y <- apply(x, 1, tmp.fct)

} else {

tmp.fct <- function(x) eta0 + calib.surf[[temp]](x)

colnames(x) <- cond

y <- tmp.fct(x)

}

# Estimate the gam model

form <- as.formula(paste0("y", tmpform))

dd <- data.frame(y, x)

names(dd) <- c("y", cond)

b <- gam(form, data = dd)

# plot(x[,1],(y-fitted(b))/y)

# Create a dummy gamBiCop object

tmp <- gamBiCopFit(data = data, formula = form, family = 1, n.iters = 1)$res

# Update the copula family and the model coefficients

attr(tmp, "model")$coefficients <- coefficients(b)

attr(tmp, "model")$smooth <- b$smooth

attr(tmp, "family") <- family

if (family == 2) {

attr(tmp, "par2") <- 2 + exp(rnorm(1))

}

model[[count]] <- tmp

count <- count + 1

}

}

## Create the gamVineCopula object

GVC <- gamVine(Matrix = Matrix, model = model, names = nnames)

print(GVC)

#> GAM-Vine matrix:

#> [,1] [,2] [,3] [,4]

#> [1,] 2 0 0 0

#> [2,] 3 3 0 0

#> [3,] 4 4 4 0

#> [4,] 1 1 1 1

#>

#> Where

#> 1 <-> X1

#> 2 <-> X2

#> 3 <-> X3

#> 4 <-> X4

#>

#> Tree 1:

#> X2,X1: Gumbel type 3 (survival and 90 degrees rotated)

#> X3,X1: Gaussian

#> X4,X1: Gumbel type 1 (standard and 90 degrees rotated)

#>

#> Tree 2:

#> X2,X4|X1 : Gumbel type 1 (standard and 90 degrees rotated) copula with tau(z) = (exp(z)-1)/(exp(z)+1) where

#> z ~ s(X1, k = 10, bs = "cr")

#> X3,X4|X1 : Gumbel type 2 (standard and 270 degrees rotated) copula with tau(z) = (exp(z)-1)/(exp(z)+1) where

#> z ~ s(X1, k = 10, bs = "cr")

#>

#> Tree 3:

#> X2,X3|X4,X1 : Gumbel type 4 (survival and 270 degrees rotated) copula with tau(z) = (exp(z)-1)/(exp(z)+1) where

#> z ~ s(X1, k = 10, bs = "cr") + s(X4, k = 10, bs = "cr")

#

if (FALSE) { # \dontrun{

### Simulate and fit the model

sim <- gamVineSimulate(n, GVC)

fitGVC <- gamVineSeqFit(sim, GVC, verbose = TRUE)

fitGVC2 <- gamVineCopSelect(sim, Matrix, verbose = TRUE)

### Plot the results

par(mfrow = c(3, 4))

plot(GVC, ylim = c(-2.5, 2.5))

plot(fitGVC, ylim = c(-2.5, 2.5))

plot(fitGVC2, ylim = c(-2.5, 2.5))

} # }